ISLAMABAD : The Federal Cabinet has reportedly refused to allow Federal Board of Revenue (FBR) to opt for Ordinance to implement policy measures to improve tax compliance including the outright confiscation of goods where tax stamps had not been affixed as well as to entrust powers to officers of the Federal and Provincial Governments to seize goods without tax stamps, sources told Newzshewz.

The Cabinet presided over by the Prime Minister, Shehbaz Sharif has directed FBR( Revenue Division) to table a Bill in the Parliament to get its nod on harsh policy measures, the sources added.

On December 2, 2024, the Cabinet was apprised that the Federal Board of Revenue (FBR) is the lead revenue-collecting agency and has embarked upon a transformation process to adopt This effort was international best practices for a better governance of collecting taxes. This effort was necessitated by the fact that Pakistan’s tax-to-GDP ratio was the lowest in the region, despite high tax rates and numerous reform efforts in the past. In order to make the tax machinery more efficient and to make the tax system more equitable, the FBR needed to embark upon a transformation plan focusing on broadening and deepening the tax base.

It was further apprised that after thorough research and consultations, a short to medium term transformation plan had already been approved by the Prime Minister, in principle. One major part of the envisaged transformation was changes in the enforcement provisions of different tax laws, for which new legislation is required. The objective of such amendments is to align the legal provisions with digitalisation, data triangulations, and taxpayer facilitation using artificial intelligence, and by plugging tax leakages.

It was informed that, accordingly, certain amendments were being proposed in the taxation laws, which envisaged enhancing the efficacy of tax collection mechanisms as opposed to the traditional mode based on increase in tax rates.

It was further apprised that the existing provisions of the Income Tax Ordinance, 2001 provided for higher rates of advance withholding taxes for persons who did not file their income tax returns, which were meant to encourage filing of returns and thereby improve tax compliance. However, a tendency had been noted that a return was filed before making transactions to avoid higher rates of withholding tax, but thereafter the person stayed as non-filer in subsequent tax years, it was therefore envisaged that instead of a higher rate of tax, restrictions on making transactions may be imposed on persons who do not have the financial capacity, as per their wealth statement or financial statement, as the case may be, to make such transactions, as detailed at paragraph 3.1.1 of the working paper submitted to the Cabinet. Similarly, in order to expand and complete value chains for efficient functioning of Sales Tax and to tackle the pervasive problem of non-registration, various proposals had been worked out.

The Cabinet was further apprised that the requirement to integrate all service providers with the Point of Sale (PoS) system of the FBR was also proposed to be implemented through amendments in Islamabad Capital Territory (Tax on Services) Ordinance, 2001 for Islamabad Capital Territory.

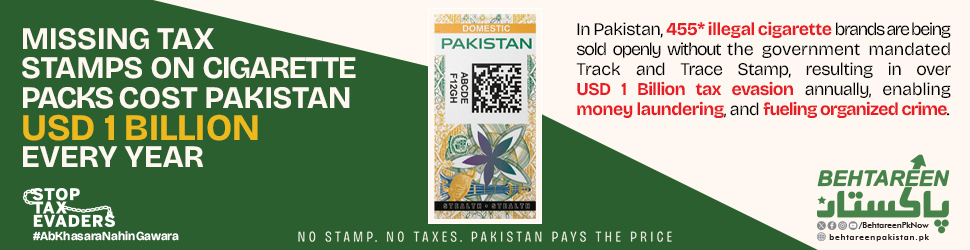

The Revenue Division informed that in order to gear increase the use of digitalisation tools, certain amendment in Central Excised Act 2005 were being proposed, as to provide for the outright confiscation of goods where tax stamps had not been affixed as well as to entrust powers to officers of the Federal and Provincial Governments to seize goods without tax stamps affixed thereon. It was further informed that the necessary amendments in the light of the directions of the Prime Minister, had been incorporated.

During the ensuing discussion, the Cabinet advised that in the case of provincial officers the FBR should take permission from the respective Provincial Governments.

The Cabinet was also of the view that the proposed amendments in the Sales Tax Act, 1990, the Islamabad Capital Territory (Tax on Services) Ordinance, 2001, the Income Tax Ordinance, 2001 and the Federal Excise Act, 2005 should not be promulgated through an ordinance, as had been proposed by the Revenue Division, but must be introduced in Parliament in the form of a bill.

After detailed discussion, the Cabinet the proposal w with the modification that the proposed amendments will be introduced in Parliament in the form of a bill, and not promulgated through an Ordinance.

Ends

{kind=link}